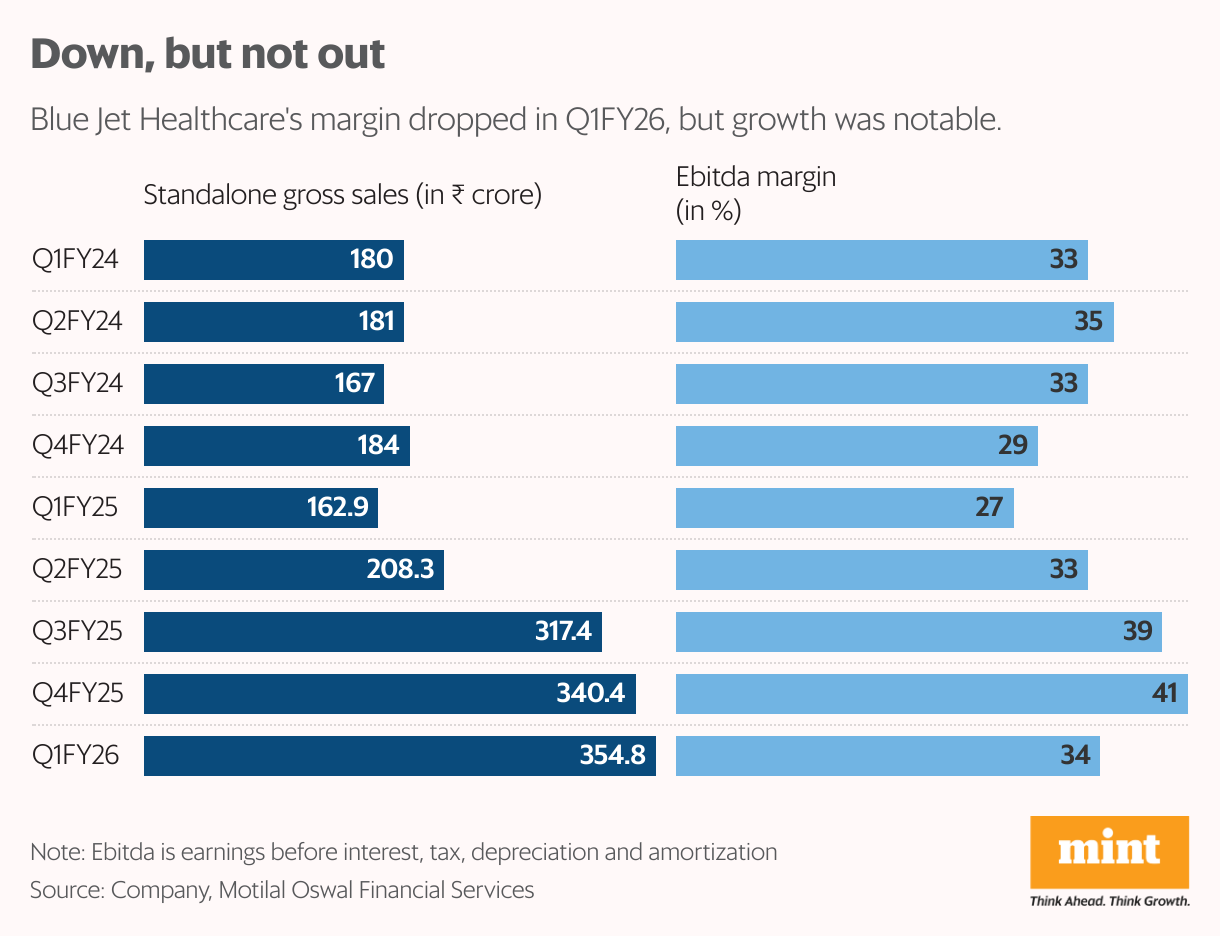

The Blue Jet Healthcare Ltd stock is down almost 40% from its 52-week high of ₹1,027.80, seen on 21 July, a day before its June quarter (Q1FY26) results were announced—showing that its Ebitda margin fell to 34% from 41% in Q4FY25 due to inventory adjustments and a little product mix shuffle.

Margins could well recover ahead, but investors will need proof before allocating brownie points. Within contract manufacturing, Blue Jet focuses on niche areas such as contrast media intermediates for diagnostic imaging, supplying major companies including GE Healthcare, Guerbet Group, and Bracco Imaging.

It also produces high-intensity sweeteners, such as saccharin, for companies like Colgate-Palmolive and Unilever, along with other speciality pharmaceutical ingredients and APIs.

Smart moves

The pharma company has been smartly moving up the value chain. In the contrast media business, it is shifting from simple building blocks to advanced intermediates, essentially extracting more value from each molecule and making it harder for others to swoop in and capture profits.

It is also undertaking backward integration at its Mahad (Maharashtra) facility, building a plant to produce a starting material it used to import. The plant is expected to commence operations in H2FY26 and boost margins.

In pharma intermediates and APIs, Blue Jet is focusing on high-margin projects in chronic therapy areas such as cardiovascular, oncology, and CNS. The upshot: This segment grew more than 4X in FY25, largely thanks to a cardiovascular intermediate developed with an innovator.

By targeting high-growth, high-margin businesses with significant entry barriers, the company is positioning itself for better growth, and once this starts showing up, there will be room for a rerating.

Over the past four years, Blue Jet has quadrupled its capacity. Revenue and profit after tax have more than doubled from ₹499 crore in FY21 to ₹1,030 crore in FY25, and from ₹140 crore to ₹305 crore, respectively. This was achieved without raising any external capital (excluding the public listing), thanks to a high-margin and capital-light business model.

It plans to add another 1,000KL capacity, supporting its medium-term goals and backed by client lock-ins.

Valuations have corrected and no longer appear as steep, even though past growth may seem somewhat slow to some investors. The stock trades at 23X FY27 estimated earnings, according to Bloomberg.